Retirement

Contact Information

Kim Coats Tuck - Retirement Specialist

[email protected] | Contact Form

(817) 540-0108 ext. 8029

Retirement Hotlines

6.12.26 – 6/10/26 APFA Virtual Retirement Town Hall Recording

This week, APFA hosted a retirement town hall. If you were unable to join the virtual meeting, please click here for a recording

6.10.26 – Reminder: 6/10/26 APFA Virtual Retirement Seminar Begins Soon!

APFA Virtual Retirement Seminar Begins Soon! Wednesday, June 10, 2026 APFA’s Virtual Retirement Seminar will be held today, from 11am to 1pm CT. Topics will include: 401(k) ● 65-Point Plan…

6.08.26 – Virtual Retirement Seminar – Wednesday, June 10, 2026

Join us for a Virtual Retirement Seminar on Wednesday, June 10, 2026 at 11:00a CT. Click here to submit your questions in advance. Join the Virtual Town Hall via Cell Phone or Tablet

5.07.26 – APFA Virtual Retirement Seminar – Wednesday, June 10, 2026

Upcoming Virtual Retirement Seminar on June 10, 2026 from 1100CT-1300CT. Click here to submit your questions in advance. A recording will be posted on the APFA Town Hall page a few days following the virtual seminars.

2.24.26 – Today’s APFA Virtual Retirement Seminar Begins at 11 AM (CT)!

We are holding a virtual retirement seminar today Tuesday, February 24, from 11 AM until 1 PM (CT). Topics will include: 401(k), 65-Point Plan, COBRA, Medicare, Pensions, Retiree Travel, RHRA, Social Security, Vacation/Sick Payout

2.23.26 – APFA Virtual Retirement Seminar Tomorrow

We are holding a virtual retirement seminar tomorrow Tuesday, February 24, from 11 AM until 1 PM (CT). Topics will include: 401(k), 65-Point Plan, COBRA, Medicare, Pensions, Retiree Travel, RHRA, Social Security, Vacation/Sick Payout. Click here to submit your questions in advance.

2.12.26 – APFA Virtual Retirement Seminar – Tuesday, February 24, 2026

We are holding a virtual retirement seminar on Tuesday, February 24, from 11 AM until 1 PM (CT). Topics will include: 401(k), 65-Point Plan, COBRA, Medicare, Pensions, Retiree Travel, RHRA, Social Security, Vacation/Sick Payout

11.11.25 – APFA Virtual Retirement Seminar Recording from Tuesday, November 11

Today, we hosted a Virtual Retirement Seminar that covered important topics such as 401(k) plans, retiree travel, sick leave and vacation, Medicare, the Retiree Health Reimbursement Arrangement (RHRA), and Social Security benefits.

This week, APFA hosted a retirement town hall. If you were unable to join the virtual meeting, please click here for a recording

APFA Virtual Retirement Seminar Begins Soon! Wednesday, June 10, 2026 APFA’s Virtual Retirement Seminar will be held today, from 11am…

Join us for a Virtual Retirement Seminar on Wednesday, June 10, 2026 at 11:00a CT. Click here to submit your questions in advance. Join the Virtual Town Hall via Cell Phone or Tablet

Start Early!

Get Started on Saving

Learn about the importance of starting to save for retirement as early as possible as well as how much to save, what funds to invest in, and taking advantage of your employer match.

Retirement Seminars

Upcoming Seminars

This week, APFA hosted a retirement town hall. If you were unable to join the virtual meeting, please click here for a recording

APFA Virtual Retirement Seminar Begins Soon! Wednesday, June 10, 2026 APFA’s Virtual Retirement Seminar will be held today, from 11am…

Past Seminars

Retirement Planning

Contact and Resources

Download a list of helpful contact and resources for Social Security, Medicare, AA Human Resources, Benefits Service Center, Medical Insurance, Prescription Drugs, Optional Insurance, MetLife, Long-Term Care, Pension Benefits, and Miscellaneous.

Eligibility: 65 Point Plan

Being eligible to retire and being eligible for a pension/social-security are different thresholds.

For retirement eligibility, American Airlines uses standard and simplified criteria based on a 65 Point Plan. Simply put, you must have at least 10 years of company service and your age plus years of company service must equal 65 or more when you leave. Eligibility can be confirmed by calling Retiree Services at (844) 543-5747 or reaching out to your FSM.

Not Yet Eligible to Retire?

Stall

One of the major advantages to being an APFA Flight Attendant is the flexibility. You can go many months/years with little or no flying. If you are close, but not quite yet eligible to retire, you can “stall” your departure date, by dropping trips (down to 40 hours,) VLOA, and various personal leaves. If you are sick, and you can provide medical substantiation for your illness, you can stay on the sick list for as long as you have sick time, plus five years (60 months) of unpaid sick. Many people getting ready for retirement, get all their necessary medical treatments done prior to retirement and losing their active employee health insurance. For many people, these delays allow enough time to become eligible to retire.

Quitting

You are free to just walk away from American Airlines at any time. You simply give notice to your Flight Service Manager. Sick time is lost. Your unused vacation is paid out at the same formula as a retiree (see previous section.) Based on your eligibility and vesting, you may be able to commence your pension (if applicable) at some point in the future. You are eligible to continue active insurance thru COBRA (see page 24).

Retiree Checklist

Vacation & Sick Time

American will pay you $8.65 for each hour of sick time left in your bank in the form of a cash payout.

Flight attendants retiring with seven or more days of vacation will receive 4.00 hours of flight pay for each day. The payout for less than seven days is 3.50 hours per day. Flight attendants have the option of participating in the vacation buy-back program each year. The payout for vacation buy back mirrors the formula used for vacations during a bid month.

Retirement Gift

Retirees are eligible to select a gift from the retirement catalog. You can also choose to donate to the WINGS Foundation in lieu of a gift. Catalogs are special ordered by your Flight Service Manager and sent to you approximately 30 days after you retire. Contact your FSM during your last 30 days and remind them to request the catalog.

Retiree Status

Upon retirement, you can request a Retiree ID from the company by completing an online form and uploading a picture. There is also a link on AA Retiree website. Airline retirees are still afforded many of the discounts they enjoyed as active employees at various hotel and rental car chains as well as shipping discounts with FedEx. The Retiree ID is not intended to replace a government issued photo ID when traveling or passing thru TSA security screening.

The loss of your Crew Member ID will also mean the loss of “crew line” expedited service thru TSA Security checkpoints and Customs and Border Patrol. The TSA Pre-Check Program and Global Entry are two programs administered by the Federal Government that allow you, for a fee, expedited passage thru these checkpoints. Non-revs are frequently designated with “Pre-Check” on their boarding passes. Enrolling in the Pre-Check program will get that designation most of the time.

Retirees have access to the AA Retirees site and (888) WE-FLYAA for checking loads and listing for flights. On the AA Retirees site, you can also update contact information, complete annual enrollment for Retiree Medical Plans and COBRA, and update non-rev traveler information.

Access to the combined Payroll system that went into effect on 10/15/2020, Epays, or Paperless Pay (for older pay data) continues thru links on the AA Retiree website.

Retiree Travel

Retiree Travel Program Benefits

The Retiree Travel Program includes the following benefits:

- Six (6) one-way D1 passes per year for the retiree and each eligible traveler (Spouse, Domestic Partner*, Registered Companion*, Children under age 24)

- Unlimited D2R travel for the retiree and each eligible traveler

- Unlimited D2P travel for the retiree’s Parents or In-laws* (D2R when traveling with the employee)

- Eight one-way D3 guest passes

- Unlimited AA20 (20% discounts of AA full fares) travel

- 20% off AAdvantage award redemptions

- ZED fare travel per specific carrier agreements (myIDtravel in AA Retirees site)

*imputed income may apply

Imputed Income

Some travelers generate “imputed taxable income.” These include:

- Registered Companions

- Domestic Partners

- All non-dependent children age 19-23

- In-laws/Domestic Partners’ parents

Retirees and former employees with travel privileges and their eligible travelers fly free in all cabins on American Airlines and American Eagle flights. International taxes and fees are charged to the traveler. (NOT INCLUDED: jumpseat travel, reciprocal cabin seat travel)

Retirees will retain access to the Travel Planner via the AA Retirees Site for checking loads, making flight listings, and placing themselves and their registered travelers on the standby list. The site also has a link to myIDtravel for purchasing and self-ticketing ZED fares on other carriers.

Airline friendly travel agencies such as Perx and Dargal also extend travel discounts to airline retirees.

Paying for Travel Charges

While travel is free, retirees will still be responsible for government taxes and airport fees, depending on the destination, as well as any service charges for D2P and D3 travel. All charges are paid via credit card, with specific card information provided when the listing is made on Travel Planner. You can even use the traveler’s credit card instead of your own. Email [email protected] for travel charge queries.

Retirement Income

You have several sources of income in retirement: 401k, Pension (LAA pre-2012 hires, LUS pre- 2/1/05 hires with a pension), Social Security, QPSA (LAA) / QDRO, Individual Retirement Accounts (IRA), and Savings

American Airlines 401k

The most effective and commonly used retirement savings tool is a 401k account. But it's only good if you take advantage of it. As Flight Attendants, we have the ability to contribute to either:

- A PRE-TAX REGULAR 401K account that earns investment returns tax free until it is withdrawn.

- A ROTH 401K account where all future investment earnings are tax free, but what you contribute goes in as a post-tax contribution.

The maximum employee contribution for 2026 is $24,500 with an additional $8,000 allowable “catch up” contribution for those over 50. A 401k plan has an unbeatable combination of advantages - payroll deduction and employer contributions.

Catch up contributions and regular contributions are deducted concurrently. Please keep this in mind at the end of the calendar year, as your Catch-Up contributions will continue in the New Year unless you reset the field to ZERO on your Fidelity Contribution page.

Match and Contribution: 5% contribution and up to a 4% match start after one year of service.

Investing in a 401k is a wise thing to do. If you don't know where to start, or are unsure about what options are right for you, Fidelity Brokerage Services has resources and tools at http://netbenefits.com/aa.

Pay Eligible for Contribution and Match

What kind of pay is eligible for the contribution and match from the company?

- Flight Pay and Credit

- Deicing, Diversion and ATC pay

- Special Assignment Pay

- Training Pay

- Holding/Ground Time Pay

- Understaffing Pay

- Purser Pay

- Galley Pay

- International Override Pay

- Language Pay

- Bid Denial Pay

- Training Stipend Pay

- Profit Sharing

401k Basics

Paycheck Contribution Limits

Automatic payroll deductions are up to 100% of eligible pay, up to annual IRS limits.

Eligibility for Employer-Matching Contributions

All employees become eligible for the employer-matching contribution after completion of one year of service.

Vesting Schedule for Employer Matching Contributions

You will become eligible for company match and contributions on your one-year anniversary and will become 100% vested (your money to keep) after two years of vesting service.

Fidelity Brokerage Link

You can set up a self-directed brokerage account, as one of the options in your 401k. This allows you to invest in almost any tradable security on US stock exchanges.

Commission Fees

The online commission rate for trade in a self-directed brokerage account is currently $0 per trade.

Loan Provisions

A participant may have up to two loans. After paying off an outstanding loan, participants must wait 30 days before a new loan can be requested. A loan default will count toward your “two loan” maximum. The interest rate for all loans will be prime + 1% based on published rates by Reuters. The minimum balance to request a loan is $2,000 and the minimum amount that can be borrowed is $1,000. The maximum loan is 50% of your balance up to $50,000. General loans have a term of 12 to 60 months, home loans have a term of 12 to 360 months.

401k Freeze

Upon termination from the company, the plan will be frozen for 30 days, after which, the participant may request a distribution, rollover, or make investment changes.

Contribution Percentage

All elections must be made in half percentage increments (example; 4.0%, 4.5%). (Previous elections made in tenths will remain in effect until you make a contribution change.)

Hardship Withdrawals

Any hardship withdrawal will result in a contribution suspension of six months, at which time contributions will resume automatically.

Account Statements

Statements will be available online only, unless the participant specifically requests a paper copy.

Roth Conversion

401k Plan Participants have the option of converting pre-tax assets from their 401k into a Roth account within the same 401k. Call the Fidelity Service Center for details.

If you have an outstanding loan at the time of your separation, AA will allow you to continue to pay back the loan per the original terms of the amortization schedule. If you decide to take a total distribution via cash out or rollover, your outstanding loan will default and become a taxable distribution. If you are under 59.5, you will also be assessed an early withdrawal penalty. Talk to your financial planner about what to do with this money. Contact information for Fidelity is at the back of this packet.

Pensions

NOTE: We hope you find this information helpful. Keep in mind, it is offered for your assistance and guidance only. Please be sure to check everything in the contract (CBA) and in Jetnet. Check with your financial and legal advisers before making any decisions. APFA and/or its representatives are not your attorney or your financial adviser. These handouts and/or these briefings do not create any obligation or rights. Certain information in this handout is also unique to each legacy carrier and will be identified with LAA or LUS.

Legacy US Pensions (LUS)

Legacy US Pensions are administered by the PBGC. As a result, they are governed under different rules. Early pension, full pension, and the age at which you can draw your pension and still fly will vary depending on which US Airways legacy carrier you started with. Legacy US Flight Attendants with questions regarding their pensions should contact the PBGC Administration at (800) 400-7242 or visit the PBGC website. At the time of the plan’s termination in 2005, the PBGC conducted an audit for each member of the plan. All reviews, verifications and calculations were completed and formal determination letters describing the amount of pension benefits were sent to participants and beneficiaries in 2005.

| Legacy Carrier | Early Pension Age | Early Pension Reduction | Full Pension & Age |

|---|---|---|---|

| Shuttle | 52 | 3% per year prior to age 62 (max reduction of 30%) | 62 |

| Piedmont, Allegheny, US Air | 55 | 3% per year prior to age 62 (max reduction of 21%) | 62 |

| PSA | 55 | 3% per year prior to age 65 (max reduction of 30%) | 65 |

Legacy AA Pensions (LAA)

| If you leave at this age | *Are you vested? | **RES | You can start you pension at this age with this reduction |

|---|---|---|---|

| 65+ | Yes: automatic at age 65 | N/A | Unreduced Pension Immediately |

| < 65 | No | N/A | No Pension |

| < 65 | Yes | < 10 years | Unreduced Pension at 65 |

| 60+ | Yes | 10+ years | Unreduced Pension Immediately |

| < 60 | Yes | 10-15 years | Unreduced Pension @ 65, or any age 60-65 w/ Pension actuarially reduced |

| 55+ | Yes | 15+ years | Unreduced Pension @ 60, or any age 55-59 w/ Pension reduced 3% for each year less than 60 |

| < 55 | Yes | 15+ years | Unreduced Pension @ 60, or any age 55-59 w/ Pension reduced 3% for each year less than 60 |

*You are vested when you have 5 or more years of “vesting service”. Vested means your pension is “locked in”. You cannot lose it. You WILL get a pension at age 65, maybe sooner.

**You earn one full year of Retirement Eligibility Service for each calendar year you are paid 734 or more flight hours. If you had less than 734 flight hours, you get a partial year of credit = paid hours / 734.

LAA Pension Definitions

Are there choices about how my pension is paid?

Both Legacy AA and Legacy US plans share three options in how a pension is paid. The snaps shots in the following section will also show you how these options appear on the LAA and PBGC LUS pension estimates.

LAA: Single Line Annuity (SLA)

The Single Line Annuity (SLA) calculation is the highest benefit level. It is the basic calculation from which all other forms are determined. It is paid for the lifetime of the retiree but does not provide a survivor benefit and will cease upon the death of the retiree. The SLA is the default form of benefit paid to a single employee.

LUS: Striaght-Life Annuity

The PBGC refers to this as the STRAIGHT-LIFE ANNUITY. On the PBGC estimate, participants starting their pension prior to age 62 will have the option of taking their annuity with either a pre and post offset amount (Option A) or the “level-ized” option, which spreads the offset out over the participants lifetime, but offers the same monthly amount from the start of the benefit (Option C).

What are the other forms of payments?

LAA / LUS: Spouse 50% Joint Annuity

This is the automatic method of payment for a married employee. The calculation for the single lifetime annuity is done, and then a permanent reduction is applied to the calculation based upon the age of the retiree and spouse at the time of retirement. In the event of the death of the retiree, the spouse will receive a payment equal to 50% of the amount that was being paid to the employee. A married employee may elect the lifetime annuity or any of the other forms of payment; however, a notarized consent of the spouse is required. Like the Straight Life Annuity option with the PBGC, participants have the option of choosing to take this benefit either with a pre and post offset amount (Option B) or a “level-ized” amount (Option D,E,F) shown in the next section.

LAA

LUS

LUS: Joint and Survivor Annuity (50%, 75% OR 100%)

This payment method allows an employee to designate anyone as a beneficiary to receive the selected level of benefit payable in the event of the retiree predeceases the beneficiary. This method of payment also has a permanent reduction based upon age of the retiree and beneficiary. It is paid for the lifetime of the retiree and provides a lifetime survivor benefit to the beneficiary at the designated level of payment. Please note: The 75% and 100% options (Options E,F) may only be taken as a “level-ized” option with the Social Security offset factored in from the beginning of the benefit. When selecting a beneficiary who is not the spouse, only the “level-ized” options (D,E,F) are permitted.

LAA / LUS: Pop Up Option (50%, 75% OR 100%)

The “Pop Up” payment method is much the same as the Joint and Survivor Annuities described above, however, if the designated beneficiary predeceases the retiree, the amount of the pension benefit “pops up” to the amount it would have been if no beneficiary calculations had been applied. There is a slightly higher reduction in the initial calculation to pay for this.

LAA

LUS

*The PBGC only permits the 50% option in their plan (Option G).

NOTE: In the three options described above there can be no change of joint annuitant should they predecease the retiree.

LAA / LUS: Period Certain (Guaranteed for LAA: 10, 15, OR 20 Years / LUS: 5, 10, OR 15 Years)

This method also has a permanent reduction applied to the pension calculation. This method of payment is paid for the lifetime of the retiree and provides a possible survivor benefit for a specified period of time. Should the retiree pre-decease the beneficiary; the beneficiary will receive the full amount for the remaining portion of the guaranteed period. Should the beneficiary pre-decease the retiree before the end of the specified period; a new beneficiary may be named. If the retiree is still collecting their pension when the specified time has elapsed, there will be no survivor benefit. This appears as Options H, I, and J on the PBGC estimate.

LAA

LUS

LAA: Level Income Option (More Up Front)

This option (for LAA only) is designed to provide a level income during retirement by considering your Social Security benefit. The Level Income Annuity Option provides an increased monthly benefit to age 62 or Social Security Normal Retirement Age, as selected by you, when many people begin receiving Social Security benefits. The monthly benefit decreases when you reach the selected age (62 or Social Security Normal Retirement Age) even if you do not begin receiving Social Security benefits at that age. This option is always combined with another option such as a Single Life Annuity, a Joint & Survivor Annuity, or a Guaranteed Period Option.

Pension Payment FAQ

How to Apply for Your Pension

LAA

It is a multistep process. To apply for your pension: Log in to www.netbenefits.com/AA. Scroll down and under Pensions, select “American Airlines Flight Attendants Pension Plan - Team Member Services” tab (this opens in a new page). Next, select the “Collect Your Pension” tab and follow the prompts. You can also request a kit over the phone by calling the Pension Service Center at (800) 447-2000, option 1, 3, 4. (International calls 781-680-8185, Ext 44428). This needs to be done no earlier than 90 days, and no later than 45 days, prior to date you wish to begin collecting you pension. Paperwork is mailed within 7-10 days and should be returned at least two weeks before your retirement date so processing can begin on time. You can call Fidelity direct at 800-354-3412.

Contact your supervisor and tell them you are retiring and give them the date. Remind them to contact the Flight Attendant Service Center to request your Payroll Transfer Record (PTR) be cut over to Retired (RT). Don’t forget when picking your exit date, that pensions only start on the first of the month. If you retire on the second, you miss a whole month of pension payments! It is a good idea to leave at the end of the calendar month and retire on the first day of the next calendar month. There is a checklist to follow at the back of this packet.

LUS

LUS flight attendants should request their pension materials directly from the PBGC. The process should start 90 days before benefit commencement. The PBGC can be reached at (800) 400-7242 on https://www.pbgc.gov/

Taxes

Both LAA and LUS pensions are subject to withholding of federal and state (if applicable) income tax. When you request your pension kit, the paperwork will include a W4P form from the IRS. Your withholding amount is determined by the number of allowances you select. Consult with your accountant or tax advisor to determine the right number of allowances you will claim. Most pensioners will not have a good idea of their income tax liability until they have been drawing their pension for a full tax year, and other factors may contribute to what you decide to claim in allowances (such as if you are LUS and double or triple dipping). New W4P forms can always be submitted if you wish to make a change. The 1099-R tax form will be mailed to you at the beginning of the year for the previous tax year. Pensions are not considered earned wages, so they are not subject to Social Security and Medicare taxes.

Before You Complete the Pension Paperwork

When you receive your pension kit in the mail, make a copy of the paperwork before you start filling it out so you have a spare in case you make a mistake. When you have completed the paperwork, make a copy for yourself before mailing it off. Pension kits should be mailed no later than the 3rd week of the month before your retirement on the first of the next month. If you have been down more than just the airplane aisle a few times and have not already submitted your Divorce Decree or QDRO, you will need to include a copy of this paperwork with your kit. If you are widowed, you will also need to include a copy of your spouse’s death certificate. If these items are not included, your pension payments will be delayed until the documents are received. If you are planning to retire and do not have these documents, contact the county that issued them and request copies so as not to delay your pension.

Keep in mind that your pension kit will not be processed until you have officially retired or separated from the Company (or reached the month following your Double Dipping age if LUS). Your first pension check is always paid retroactively, normally about 6 – 8 weeks after you retire.

LAA: Qualified Pre-Retirement Survivor Annuity (QPSA)

Your selection of a Joint Annuitant when you request your pension, determines how you would leave your pension to a survivor once you are retired. What happens if you were to pass away before you retire? Does anyone inherit your pension?

Federal law requires that a pension plan must allow a pension to be inherited by a spouse. The default amount mandated by federal law is for the surviving spouse to get 50% of your joint and survivor pension.

APFA negotiated a better benefit. If you file a QPSA (qualified pre-retirement survivor annuity) form you can designate that your legally married spouse receives up to 100% of your joint and survivor pension should you die before you retire. For Flight Attendants, this benefit is a no cost option. If you do not fill out this form, should you die before benefit commencement, your spouse will only receive 50% of your pension. Once you make your selections for form of benefit at retirement and begin receiving pension payments, this form is replaced by your new selection. There are copies of this form at the back of this packet, the APFA website, and the Pension Service Center site on jetnet.

Qualified Domestic Relations Order (QDRO)

A QDRO is a decree from your divorce settlement that will indicate if your ex-spouse is entitled to a portion of your pension, and if so, how much. If you have gone thru a divorce during your time as an employee of American Airlines, HR will need a copy of your QDRO or Divorce Decree on file before they will initiate pension payments. The company does not pay pensions until all forms are complete and on file. If you have an LAA pension, QDRO’s on file will be have a “Yes” indication in your Plan Specific Data section of the Pension Service section on jetnet. QDRO forms can be mailed to: American Airlines HR Services, P.O. Box 14452, Des Moines, IA 50306-3452

LUS: QDRO’s must be sent to the PBGC. Visit https://www.pbgc.gov/wr/benefits/qdro for information about submitting your QDRO to the PBGC.

Social Security

Full retirement age is the age at which a person may first become entitled to full or unreduced Social Security retirement benefits. No matter what your full retirement age (also called Social Security Normal Retirement Age - SSNRA), you may start receiving benefits as early as age 62 or as late as age 70.5.

Retiring Early

You can retire at any time before full retirement age. However, if you start benefits early, your benefits are reduced a fraction of a percent for each month before your full retirement age. The following chart lists age 62 reduction amounts and includes examples based on an estimated monthly benefit of $1000 a month at full retirement age.

Pros and Cons of When to Begin Taking Your Social Security Payments

As a general rule, early or late retirement will give you about the same total Social Security benefits over a normal lifetime. If you retire early, the monthly benefit amounts will be smaller to take into account the longer period you will receive them. If you retire later, you will get benefits for a shorter period of time but the monthly amounts will be larger to make up for the months when you did not receive anything.

There are advantages and disadvantages to taking your benefit before your full retirement age. The advantage is that you collect benefits for a longer period of time. The disadvantage is your benefit is reduced. Each person's situation is different, so

- If you delay your benefits until after full retirement age, you may be eligible for delayed retirement credits that would increase your monthly benefit;

- There are other things to consider when making the correct decision about your retirement benefits.

Working and Drawing Social Security Benefits

You can work while you receive Social Security retirement (or survivors) benefits. When you do, it could mean a higher benefit for you in the future. Higher benefits can be important to you later in life and increase the future benefit amounts your family and your survivors could receive.

Note: If you are outside the United States, the rules for receiving benefits while you are working are different.

If you decide to take your benefits early, you can continue to work but you are limited in how much you can earn while getting early Social Security benefits. While you are working, your earnings will reduce your benefit amount only until you reach your full retirement age. After you reach full retirement age, Social Security recalculates your benefit amount to leave out the months when they reduced or withheld benefits due to your excess earnings.

Social Security uses a formula to determine how much your benefit must be reduced:

- If you are under full retirement age for the entire year, they deduct $1 from your benefit payments for every $2 you earn above the annual limit. For 2026, that limit is $24,480.

- In the year you reach full retirement age, they deduct $1 in benefits for every $3 you earn above the limit, but they only count earnings before the month you reach your full retirement age.

- If you will reach full retirement age in 2026, the limit on your earnings for the months before full retirement age is $62,160.

- Starting with the month you reach full retirement age, you can get your benefits with no limit on your earnings.

Are Social Security Benefits Taxable?

The short answer is maybe. For a complete answer, visit the IRS Website. Social Security Estimated Benefits paper statements are no longer mailed annually. Electronic versions are available at any time via the Social Security website. Sign up and register today at http://ssa.gov.

Other Retirement Income

Individual Retirement Accounts (IRA)

An Individual Retirement Account is a type of "individual retirement plan", offered by many financial institutions. It provides tax advantages for retirement savings in the United States. There are two main types of IRA accounts:

- Traditional IRA – contributions are “before tax” and grow untaxed until you withdraw the money. Withdrawals at retirement are taxed as income.

- Roth IRA – contributions are made “after-tax”, and grow untaxed. Withdrawals (including interest) are tax free in retirement.

Contribution Maximums: For 2026, the maximum contributions for both the Traditional IRA and the Roth IRA are $7,500 with an extra $1,000 for individuals over 50 years of age.

Imcome Limits: You can contribute the maximum to a Roth IRA in 2026 only if your adjusted gross income is less than $153,000 if single or $242,000 if married filing jointly.

Tax Credits: Individuals with lower incomes can file a Retirement Savings Contribution Credit on their income taxes. Visit http://www.irs.gov/taxtopics/tc610.html for more information.

| 2026 Saver's Credit | |||

|---|---|---|---|

| Credit Rate | Married Filing Jointly | Head of Household | All Other Filers* |

| 50% of contribution | AGI up to $48,500 | AGI up to $36,375 | AGI up to $24,250 |

| 20% of contribution | $48,501 - $52,500 | $36,376 - $39,375 | $24,251 - $26,250 |

| 10% of contribution | $52,501 - $80,500 | $39,376 - $60,375 | $26,251 - $40,250 |

Savings

Personal savings for each person will vary based on individual circumstances. Savings can include, but are not limited to Equity in your home, Life Insurance, Inheritance, Saving Accounts and Certificates of Deposit (CD’s). While there is no minimum required amount, it’s important to have an adequate savings base to complement your other income holdings. The consensus is that your savings should be able to cover a minimum of three to six months of living expenses. A Financial Advisor can give you recommendations on how to have a healthy portfolio.

Previous Early Out Offerings

Post-Retirement Health Benefits

Start Here: Are You Eligible For Medicare?

Medicare

Retiree medical insurance is not available to you once you turn 65, and COBRA is considered secondary to Medicare. Unless you are going on some other active medical insurance that is considered creditable coverage by Medicare, you will be enrolling in Medicare. If you will be 65 or older at your exit date, you will want to begin researching the type of coverage you will want to purchase with Medicare. There are numerous books on Medicare as well as lots of information on the Medicare website at www.medicare.gov. If you are eligible for early Medicare as the result of a disability, do not sign up for the American Airlines Retiree Medical Plan or elect COBRA. Medicare is as easy as A B D!

Medicare Part A:

Covers hospitalization

Medicare Part A covers inpatient hospital, skilled nursing facility, and some home health care services and for most people has been prefunded. About 99 percent of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment.

Medicare Part B:

Covers physician care

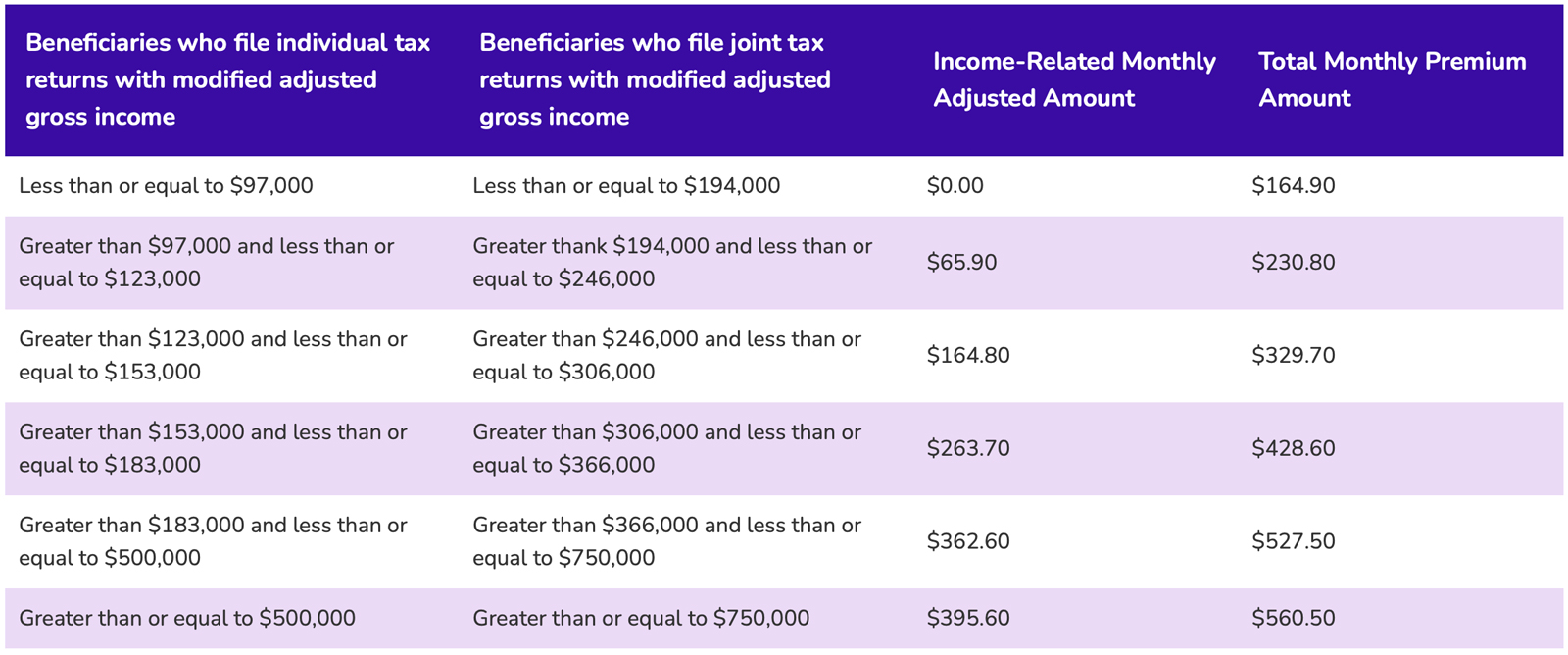

If modified adjusted gross income as reported on your IRS tax return from 2 years ago (the most recent tax return information provided to Social Security by the IRS) is above a certain amount, you may pay more.

Medicare Part D:

Covers prescription drug benefits

Medicare offers prescription drug coverage to everyone with Medicare. To get Medicare drug coverage, you must join a plan run by an insurance company or other private company approved by Medicare. Each plan can vary in cost and drugs covered.

Late Enrollment Fees

Medicare Part B and D have late enrollment fees of 10% per year for each year you delay signing up for coverage after age 65. Retiring flight attendants over age 65 can waive these fees by showing they had employer sponsored coverage when they first enroll. The two ways to do this are with a Letter of Credible Coverage from the Benefits Service Center or having AA complete the Employer Verification Form.

Medicare Supplemental (Medigap) Insurance

Medicare supplement (Medigap) insurance, sold by private companies, can help pay some of the health care costs that Original Medicare doesn’t cover, like copayments, coinsurance, and deductibles. Some Medigap policies also cover medical care when you travel outside the U.S. If you have Original Medicare and you buy a Medigap policy, Medicare will pay its share of the Medicare-approved amount for covered health care costs. Then your Medigap policy pays its share.

Airline Retiree VEBA

Retiring Flight Attendants who are 65 and over may take advantage of an Airline Retiree Medicare Voluntary Employee Beneficiary Association (VEBA) to help pay for out of pocket costs associated with Parts A, B and D. The VEBA Retiree Services number is (888) 287-4101. Their current Benefits Guide is available for download from the Retirement page at apfa.org.

All of the information below is found on the Medicare website at www.medicare.gov. Make sure you shop a variety of Medigap and Part D drug plans to make sure you get the plans that are right for your needs. There is a plan finder on the Medicare website.

NOTE: A Medigap policy is different from a Medicare Advantage Plan. Those plans are ways to get Medicare benefits, while a Medigap policy only supplements your Original Medicare benefits.

How do I compare Medigap policies?

If a percentage appears, the Medigap plan covers that percentage of the benefit, and you’re responsible for the rest. Visit Medicare.gov to see the 202 benefit amounts.

* Plans F and G also offers a high-deductible plan in some states. With this option, you must pay for Medicare-covered costs (coinsurance, copayments, and deductibles) up to the deductible amount of $2,700 in 2023 before your policy pays anything. (Plans C and F won’t be available to people who are newly eligible for Medicare on or after January 1, 2020. See previous page for more information.)

** For Plans K and L, after you meet your out-of-pocket yearly limit and your yearly Part B deductible, the Medigap plan pays 100% of covered services for the rest of the calendar year.

*** Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission.

Eight Things to Know About Medigap Policies

- You must have Medicare Part A and Part B.

- If you have a Medicare Advantage Plan, you can apply for a Medigap policy, but make sure you can leave the Medicare Advantage Plan before your Medigap policy begins.

- You pay the private insurance company a monthly premium for your Medigap policy in addition to the monthly Part B premium that you pay to Medicare.

- A Medigap policy only covers one person. If you and your spouse both want Medigap coverage, you’ll each have to buy separate policies.

- You can buy a Medigap policy from any insurance company that’s licensed in your state to sell one.

- Any standardized Medigap policy is guaranteed renewable even if you have health problems. This means the insurance company can’t cancel your Medigap policy as long as you pay the premium.

- Some Medigap policies sold in the past cover prescription drugs, but Medigap policies sold after January 1, 2006 aren’t allowed to include prescription drug coverage. If you want prescription drug coverage, you can join a Medicare Prescription Drug Plan (Part D).

- It’s illegal for anyone to sell you a Medigap policy if you have Medicare Medical Savings.

Medicare Advantage Plans (Part C)

Another option is buying your Medicare through a Medicare Advantage Plan, commonly called a Part C plan. This essentially rolls your Part A, B and (in some cases) D plans into an HMO or PPO administered by a private insurance company. You can choose the plan that fits your needs, and in some cases, attach additional benefits to the plan such as vision, hearing, and dental. In addition to your Part B premium, you will have a monthly premium for your Advantage plan. It’s best to consult a Medicare Broker if going this route as you want to make sure you choose a plan that works for you and includes the doctors you visit and the prescription drugs you take.

What is a Medicare health plan? A plan offered by a private company that contracts with Medicare to provide Part A and Part B benefits. Health plans include all Medicare Advantage Plans, Medicare Cost Plans, Demonstration/Pilot Programs, and Programs of All-inclusive Care for the Elderly (PACE). With Medicare Advantage Plans, you’re always covered for emergency and urgently needed care. Medicare Advantage Plans must cover all of the services that Original Medicare covers except hospice care

The plan can choose not to cover the costs of services that aren’t medically necessary under Medicare. If you’re not sure whether a service is covered or not, check with your provider before you get the service.

Non-Medicare Options

Not Medicare Eligible Yet

Consolidated Omnibus Budget Reconciliation Act (COBRA)

You may continue your active medical insurance thru COBRA for 18 months after you leave the company. You have 60 days from your last day of employment to make your COBRA elections, so make sure that you don’t miss the deadline. In addition, COBRA coverage may be extended an additional 11 months, up to a maximum of 29 months, for Flight Attendants who qualify for Social Security Disability.

Continuation of Coverage (COBRA)

If your employment terminates for any reason (i.e., furlough, resignation, etc.), your active medical is cancelled, along with your other benefits. You may elect to continue your health benefits as part of your continuation of coverage options available through Alight, the COBRA administrator. Alight will mail a COBRA package to your home address (or to the address you provide) after your termination is processed. If you do not continue your active medical through COBRA, claims incurred after the date of your termination are not payable.

Several of American Airlines’ other benefits or plans (Dental Benefits, Vision Insurance Benefits, and Health Care Flexible Spending Accounts) provide for continuation of coverage under the COBRA in case of certain Qualifying Events. If you and/or your dependents have coverage at the time of the Qualifying Event, you may be eligible to elect continuation of coverage under the following:

- Medical Benefits

- Dental Benefits

- Vision Insurance Benefits

- Health Care Flexible Spending Account Benefit: for the remainder of the calendar year in which you became eligible for continuation of coverage. (Although you would not be able to make contributions on a pre-tax basis, by electing continuation of coverage for this account, you would still have the opportunity to file claims for reimbursement based on your account balance for the year.)

The coverage under COBRA is identical to coverage provided under the benefits or plans for active employees or their dependents, including future changes.

Cost of COBRA Coverage for 2026

| Self-Funded Medical | Employee Only | Employee & Spouse | Employee & Children | Employee & Family |

|---|---|---|---|---|

| High Cost Coverage | $2,087.65 | $4,801.62 | $3,757.75 | $6,471.71 |

| Standard | $964.20 | $2,217.66 | $1,735.55 | $2,988.98 |

| Core | $857.11 | $1,971.34 | $1,542.79 | $2,657.06 |

| DFW Connected Care | $588.37 | $1,354.09 | $1,059.71 | $1,825.06 |

| Plus | $951.14 | $2,187.60 | $1,712.07 | $2,948.49 |

| Dental | ||||

| Basic Dental | $28.63 | $59.25 | $64.13 | $101.35 |

| Plus Dental | $39.76 | $82.30 | $89.09 | $140.76 |

| Vision | ||||

| $7.19 | $13.93 | $13.68 | $19.56 | |

Alight

Alight is the COBRA billing administrator and handles solicitation and enrollment. You will receive a COBRA solicitation via mail within two weeks following your retirement. If you continue active coverage through COBRA, you will have no lapse of coverage of medical insurance, but until the coverage is entered into the system upon your enrollment, you will pay for medical care out of your pocket and apply for reimbursement.

Complete and mail the election form back to Alight. Once they receive the election notice, their system will be updated within 72 hours to show the elections. After elections are in the system you can make a payment. Once the payment is made and posted, eligibility will be sent to your claims administrators.

Over age 65?

Cobra is not considered credible coverage as defined by Medicare, and will become secondary coverage to Medicare. If you are 65 or older when you retire, Medicare will become your primary coverage. Check with legal and financial advisers about medical coverage options if you are over 65 to avoid substantial financial penalties/reduction in coverage if you make the wrong choices!! As a rule, COBRA will only pay 20%. (Please note that Flight Attendants qualifying for early Medicare due to a Social Security Disability award will not be permitted to remain on COBRA once they reach their Medicare eligibility date).

Under COBRA, the employee does not have to reestablish deductibles. Deductibles and out-of-pocket maximums met during active employment will continue.

Since COBRA is a continuation of your active medical, the cost is the total cost of your health insurance. That means it includes what you now pay through payroll deduction, what the company pays on your behalf as part of your benefits package, plus a 2% administration fee to cover the cost of administering COBRA benefits.

It is very important to make your payments to Alight on time as once COBRA coverage is lost due to late payment it will not be reinstated!!

Per the Employee Benefits Guide, “To maintain COBRA continuation of coverage, you must pay the full cost of continuation of coverage on time, including any additional expenses permitted by law. Your first payment is due within 45 days after you elect continuation of coverage. Premiums for subsequent months of coverage are due on the first day of each month for that month’s coverage. If you elect continuation of coverage, you will receive payment coupons or invoices from Alight, Inc. indicating when each payment is due. Payments are due even if you have not received your payment coupons. Failure to pay the required contribution on or before the due date, or by the end of the grace period will result in termination of COBRA coverage, without the possibility of reinstatement.”

American Airlines Retiree Medical Insurance

Retirees between the ages 55 and 65 at separation, who meet the 65 Point Plan requirements, are eligible to purchase retiree medical insurance. You pay the full contribution cost for this pre-65 retiree medical coverage if you choose to enroll. Legacy AA Flight Attendants who retired prior to 11/1/12 continue to receive pre-funded retiree medical insurance.

The Retiree Standard Medical Plan (RSMP)

Retiree medical coverage is offered through the preferred administrator for your state. You can request a packet with enrollment information and plan details after you retire (you will also receive a COBRA solicitation. Do not confuse the two). You can only enroll in retiree medical once, any time after retirement but before age 65. For the first 30 days after separation you may enroll online. After that, just call the Benefits Service Center at (888) 860-6178. American reserves the right to amend or terminate the RSMP at any time.

Paying for Coverage

You must pay your retiree medical contributions each month by the due date. Do not be late! If your payment is late, your coverage will be terminated and you will NOT be able to re-enroll. Alight handles the billing and payment is made a month in advance. They offer an Automatic Billing feature to pay your contribution costs and ensure payments are always on time. The chart below explains the plan premiums, and maximum benefits for 2024.

| Retiree Standard | |

|---|---|

| Individual Medical Maximum Benefit | $300,000 |

| In Network Deductible | $150 per person / $400 family |

| Out of Network Deductible | $150 per person / $400 family |

| Coinsurance (In/Out) | 20% / 40% |

| In Network Out of Pocket Max (Single/Family) | $1,000 / $3,000 |

| Out of Network Out of Pocket Max (Single/Family) | $1,000 / $3,000 |

| 2026 Retiree Standard Medical Plan Premiums | |

|---|---|

| Employee Only | $2,563.00 |

| Employee Plus 1 | $5,126.00 |

| Employee Plus 2 | $7.689.00 |

Dependent Eligibility

Under the Retiree Medical Benefit, an eligible dependent is an individual who is related to the retiree in one of the following ways:

- Spouse or Company-recognized Domestic Partner

- For retirees under age 65, an eligible dependent may also include:

- Unmarried child under age 19

- Unmarried incapacitated child age 19 + who maintains legal residence with you.

- Unmarried child age 19 through 22, if the child is registered as a full-time student at a school/educational institution in a program of study leading to a degree or certification (proof of continuing eligibility will be required from time to time) and either: The child maintains legal residence with you; or You are required to provide coverage under a Qualified Medical Child Support Order (QMCSO) that is issued by the court or a state agency. If, for medical reasons, the child is required to reduce or terminate his or her studies, coverage will be continued for up to 12 months (one year). The child must be under a physician’s care and statements must be provided from the attending physician and school/educational institution to your network/claims administrator. After 12 months (one year), coverage will end unless the child returns to school school/education institution full-time or meets the definition of an incapacitated child.

If you have enrolled your dependents into Retiree Medical by the time you turn 65, when your coverage ends at 65, they continue to be covered as long as they remain eligible. You may not enroll any new dependents into the plan after you turn 65.

Retiring after age 65? If you do not start Retiree Medical by age 65, you cannot get dependent coverage for your spouse or children, regardless of their eligibility.

If you take the AA RSMP - Supplemental coverage (Back Up Plan) DO NOT CONFUSE THIS COVERAGE WITH MEDIGAP/SUPPLEMENTAL POLICIES FOR MEDICARE. THIS SUPPLEMENTAL POLICY IS A BACK UP TO AMERICAN’S RETIREE MEDICAL PLAN.

If you exhaust your AA Retiree Medical, The Supplemental Medical Plan begins and pays a percentage of eligible expenses for medically necessary care, treatment and supplies up to the usual and prevailing fee limits with a maximum medical benefit of $500,000. You must enroll when you are first eligible as a retiree and maintain coverage. The plan’s claims are processed by HealthFirst TPA (800) 711-7083. Enrollment in the plan is handled by Alight.

When does Supplemental Medical pay a benefit?

- When you or your covered spouse exhausts your maximum medical benefit under your selected Retiree Medical Benefit Option.

- If you are the surviving spouse of a retired employee who dies while you are both covered under this Plan.

What happens to my retiree medical coverage after I turn 65?

When you reach age 65, Medicare becomes your primary coverage. You will no longer be eligible for American Airlines Retiree Medical Benefits. You will be offered access to purchase a Medicare supplement plan provided by United HealthCare, a third-party vendor. You are guaranteed coverage as long as you enroll when you first become eligible, regardless of your health status. Visit United HealthCare Medicare Solutions and use the Plan Selector Tool to compare different plans and pricing options that meet your needs. Via Benefits can also provide Medicare supplement quotes and their contact info is in the back of this handout.

Affordable Care Act (ACA)

The Affordable Healthcare Act (also known as the ACA) is a government-sponsored program that allows you to purchase insurance via a state or federal exchange. Visit http://healthcare.gov where you’ll provide some information about your household size and income to find out if you can get lower costs on your monthly premiums and out-of-pocket costs for private insurance plans. You’ll see all the health plans available in your area so you can compare them side-by-side and pick the plan that’s right for you.

Major insurance companies write the policies and you are allowed to shop in the marketplace for a policy that meets your specific needs. Premiums are based on Age and Zip Code. You can preview the premium rates in your area by visiting https://www.healthcare.gov/find-premium-estimates/.

American has contracted with a nationwide third-party provider called Via Benefits. Their insurance brokers can give you quotes and enroll you in an ACA plan. Additionally, they can quote and sell you private insurance policies. Their counselors can be reached at (844) 287-9947 and you can find more information thru their website http://my.viabenefits.com/americanairlines

Based on income levels, you may also be eligible for a tax credit to help lower premiums and out-of-pocket costs. A subsidy calculator for enrollments is available at https://www.healthinsurance.org/obamacare/subsidy-calculator/

Your retirement is a Qualifying Life Event and triggers a “Special Enrollment Period”, and allows you to purchase insurance via the Healthcare Marketplace outside of set annual enrollment periods.

Other Insurances

Dental Insurance

You will be offered retiree dental insurance. The cost of the retiree dental plan is determined by the zip code where you live. In most cases COBRA coverage that offers a continuation of your active dental will be less expensive and will be better coverage. The 18 months of COBRA dental coverage will give you time to shop dental plans including the retiree dental plan. The AA credit union has a dental club that gives you a network to choose dentists who will give you a discount on services. Dental insurance is difficult to find and expensive. Nobody wants to insure old people’s teeth but there are a few alternatives that you may wish to investigate.

While original Medicare doesn’t provide dental coverage, some Medicare Advantage (Part C) plans do.

Dental discount networks also exist. You pay annual membership fees ranging from $80-$200 a year in exchange for discounts ranging from 10% to 60% from participating dentist. To find a network, visit http://dentalplans.com and search for plans and providers by zip code. The AA Credit Union offers a dental discount network as well thru Benefit Services of America. Call (866) 838-1763 or email them at [email protected] for more information.

Dental schools provide dental care from students under the supervision of licensed professors for as much as half the cost of regular services. To search for dental schools, visit http://ada.org/dentalschools.

Flexible Spending Accounts (FSA)

There are two possible scenarios concerning your flexible spending account.

- Positive Balance: You leave with funds still in the account. For example: you elect to place $2500 in your account for next year, you leave at the end of March, and you have contributed $625 at that point, but have only used $400, American gets to keep the $225 already on deposit in the account. (Pro-Tip: you could continue your flexible spending account through COBRA. Although you could not continue to contribute pretax dollars, you could use what you have already contributed.)

- Negative Balance: You leave the company before year’s end with a zero balance in your flexible spending account. You have been paid out more than you have contributed to the account. You do not have to repay American the difference. For example: you elect $2,500 in your flexible spending account for next year. In January you have dental work done which requires all $2,500 from your account. You separate from the company and retire March 31.

- At that time, you have only contributed $625 to your account through payroll deduction, but you have used $2,500. You will not have to reimburse American the difference of $1,875.

Life Events & Optional Insurance

Life Events

Federal law defines your ability and time frame in which to apply for other insurance under a spouse/partner’s plan through a life event. You have the right to request “special enrollment” in another group health plan for which you are otherwise eligible (such as a plan sponsored by your spouse’s employer) within 30 days after your Plan coverage ends. You will also have the same “special enrollment” rights at the end of COBRA coverage if you get continuation of coverage for the maximum time available to you. Keep in mind that when joining your spouse’s plan, you must re-establish all deductible and out of pocket maximums under the new plan.

Optional Insurance

You can continue these coverages by contacting the vendors directly to continue your policies: Long-Term Care insurance, Hyatt Legal Plan, and other optional coverages available through AA Added Benefits. Please refer to contact page at the back of the packet for phone numbers to discuss continuation of these types of coverage.

You can convert/(port) your AA Life Insurance and/or Accident Insurance from a group policy to an individual policy: AA does not provide Retiree Life Insurance. Your current employee term life insurance and voluntary accident insurance ends at retirement. These policies include portability and conversion rights that allow you to continue coverage as a term policy or convert coverage to a personal policy (other than term life insurance) without providing proof of good health. To port or convert Life Insurance, contact MetLife at 1-877-275-6387 within 30 days of your last day on payroll. Policies for Accidental Death & Dismemberment and Voluntary Personal Accident Insurance can be converted by calling the Life Insurance Company of North America (LINA) at 1-800-238-2125, and select option 4 and 7.

Policies you cannot continue: You cannot continue LTD and STD as they replace existing income. However, if you are receiving LTD and/or STD payments may continue if you are eligible.

APFA Headquarters

1004 West Euless Boulevard

Euless, Texas 76040

M-F: 9:00AM - 5:00PM (CT)

Phone: (817) 540-0108

Contract & Scheduling Desk

M-Th: 9:00AM - 5:00PM (CT)

Phone: (817) 540-0108

Live Chat Messaging

Fridays: 9:00AM - 5:00PM (CT)

Currently, no scheduled events...